Semiconductor Market Outlook 2026: AI Memory Squeeze, PC Price Hikes, and MLCC Supply Risks

Published: 12.26.2025

Key takeaways

- Memory remains the center of gravity with AI-driven demand pulling manufacturing capacity toward HBM and high-capacity DDR5, tightening supply for conventional DRAM/NAND used in PCs and mainstream devices.

- High-spec MLCCs are the “quiet constraint”. TrendForce flags risk concentration in new-spec, high-performance MLCCs for CSP accelerator modules and AI power rails. TrendForce

- SEMI projects equipment spending growth through 2027, signaling capacity expansion, but not necessarily fast relief for the tightest categories in 2026.

The semiconductor industry is ending 2025 with a clear divide as AI infrastructures continue to attract capital, engineering focus, and prioritized supply while consumer-facing segments remain more cautious due to softer unit demand and uneven refresh cycles.

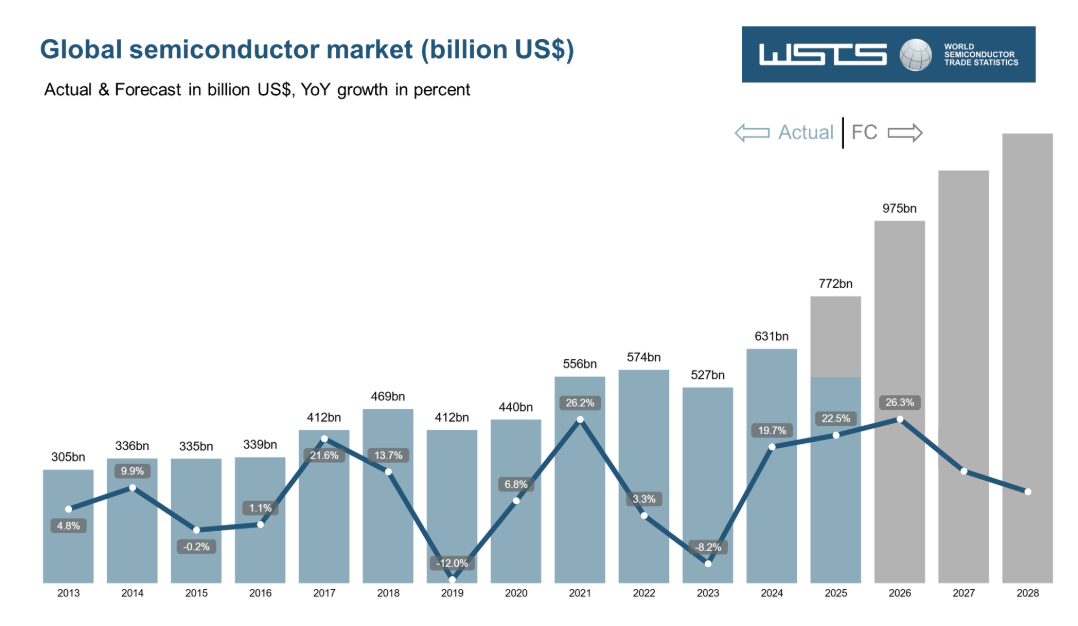

At the macro level, forecasts still point to strong expansion. WSTS projects the global semiconductor market at roughly $772B in 2025 and $975B in 2026, with Memory and Logic again leading growth.

The key operational insight is not about demand strength, but demand concentration. As growth narrows into a few high-value categories, supplier would naturally optimize for margin stability and forecast certainty reshaping allocation behavior well before shortages appear at the system level.

Pressure point: Memory Allocation is Driving Downstream Cost and Availability Risk

AI servers consume disproportionately large amounts of memory, and HBM is the most constrained segment. IDC argues the industry is experiencing a structural inflection where capacity is being reallocated away from conventional memory for consumer devices toward HBM and high-capacity DDR5 used in AI data centers.

That shift is increasingly visible in supplier strategy. Micron’s fiscal Q1 2026 results explicitly link performance to AI demand acceleration, and the company has also moved to exit its Crucial-branded consumer memory business as it refocuses on higher-margin markets.

Why this matters for PCs (and any product exposed to commodity memory)

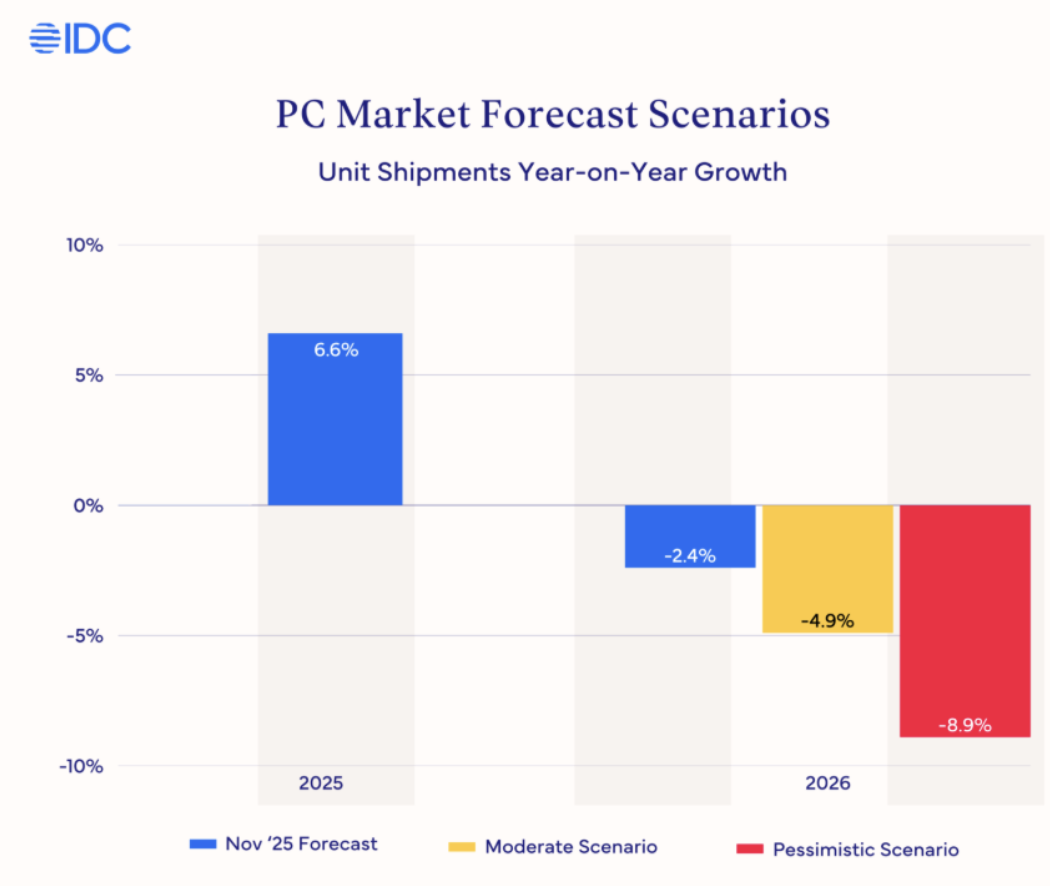

IDC outlines downside risk scenarios for 2026 that connect memory tightness to both pricing and volumes:

- Under a moderate downside scenario, IDC models the PC market contracting 4.9% (vs. a 2.4% decline in its November forecast), and PC average selling prices rising 4–6%.

- Under a pessimistic downside scenario, IDC models a contraction of 8.9% and PC ASP increases of 6–8%, depending on how long supply constraints persist through 2026.

Even with soft end-demand, PC and consumer device builds can still face price pass-through, allocation risk, and longer lead times because supply is being redirected toward AI rather than expanding evenly across end markets.

Components Story: The Constraint is Moving into Power Delivery and High-Spec Passives

As compute density rises, stress shifts beyond processors and memory into power delivery. AI platforms require stable, high-current rails, which increases demand for a narrower subset of passives with tighter electrical requirements.

TrendForce’s MLCC bulletin highlights that demand is being pulled by AI data centers and CSP-designed accelerators, with emphasis on new-spec MLCCs (including examples like 47u/100u) and yield leadership among top-tier suppliers, naming Murata in the context of yield performance and share capture.

This is where MLCC risk becomes easy to misunderstand. The constraint is not “all MLCC.” The higher risk sits in:

- high-capacitance, high-reliability, tight-spec MLCCs near advanced processors and power rails, and

- parts where second-source qualification is slower and yields can limit supply elasticity.

At the same time, CSPs are scaling custom accelerators. TrendForce notes these platforms may use fewer MLCCs than some GPU systems, but the spec and pricing profile is higher, making them strategically important for suppliers and a risk point for buyers.

Capacity is coming but 2026 still looks like a transition year

SEMI forecasts global semiconductor manufacturing equipment sales rising to $133B in 2025, then $145B in 2026 and $156B in 2027, driven by AI-led investments in leading-edge logic, memory, and advanced packaging.

Investment cycles don’t translate into immediate supply relief, particularly in constrained segments tied to advanced packaging flows, HBM ramps, and the highest-performance passive components.

Beyond demand and capacity, 2026 risk includes supply-chain disruption and tighter controls around strategic technologies. Reuters reports South Korean prosecutors have charged individuals over alleged leakage of advanced DRAM manufacturing technology to China’s CXMT—underscoring the geopolitical sensitivity around memory and AI-related capability.

IBS Electronics will continue tracking memory availability and AI-driven procurement risks across the global semiconductor market. For more updates and related industry coverage, visit the IBS Electronics Market News and stay ahead of the curve.