DRAM Shortage Risk Emerges for Automakers as AI Pulls Supply

Published: 1.30.2026

.png)

The automotive supply chain may be headed for a familiar stress point, but this time, the potential constraint isn’t MCUs. UBS is warning that tightening DRAM availability tied to the AI data-center buildout could become disruptive for automakers starting next quarter (Q2 2026), with some industry participants already acknowledging price increases of more than 100% for certain parts.

In a recent note, UBS analysts led by David Lesne flagged that a data center-driven memory squeeze is now spilling into adjacent industries, including automotive, because memory makers are prioritizing higher-margin demand and shifting capacity allocation decisions accordingly. UBS said it would not rule out “material downside risk” to global vehicle production, with disruption risk potentially starting in Q2 2026.

AI changes the DRAM allocation math

The tightening is not because automakers suddenly consume the same memory configurations as AI servers. The disruption comes from how AI reshapes the memory ecosystem itself. AI servers rely heavily on: HBM (high-bandwidth memory), which is built from stacked DRAM dies & High-capacity server DRAM, produced on similar process nodes and competing for the same capital, tooling, and engineering resources.

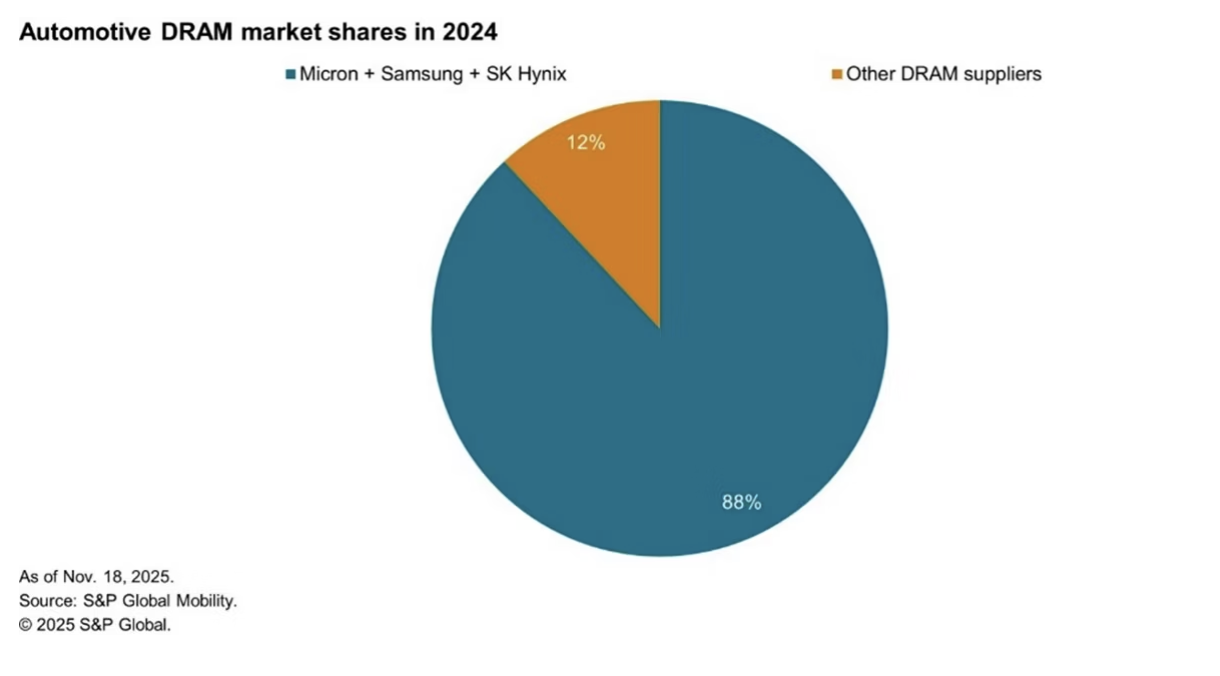

Memory suppliers including Samsung Electronics and SK Hynix have openly stated that AI demand is absorbing an outsized share of incremental capacity, with long-term contracts signed years in advance. The Financial Times reported that suppliers are prioritizing hyperscaler commitments, constraining availability for other sectors through at least 2027.

Crucially, this happens even if total wafer capacity does not collapse. As UBS frames it, allocation is the binding constraint.

As suppliers optimize for profit and long-term contracts with hyperscalers, “non-AI” segments can face tighter allocation, longer lead times, and more aggressive pricing, even when total industry wafer capacity isn’t collapsing.

S&P Global Mobility’s automotive analysis frames this as a window problem: automakers have a narrowing period to lock in supply, qualify alternates, or redesign systems before constraints become more structural.

DRAM pricing is already signaling stress

Market pricing data reinforces UBS’s warning. DRAM prices are rising sharply across both contract and

spot markets, particularly for legacy nodes still used widely in automotive electronics.

SK Hynix, the world’s second-largest memory supplier, recently posted record profits driven by AI-related memory demand and acknowledged strong upward pricing momentum in DRAM . Reuters reported that some DRAM categories have already seen dramatic price increases, reflecting tight supply conditions.

UBS notes that some industry participants are already acknowledging price hikes of more than 100% for certain components. Even when automakers can technically secure supply, the cost shock alone can disrupt negotiations and production planning.

UBS modeled a simplified stress case showing that a +120% DRAM price increase, with 80% OEM cost recovery, could still translate into a 5% EBIT hit for a generic supplier in 2026.

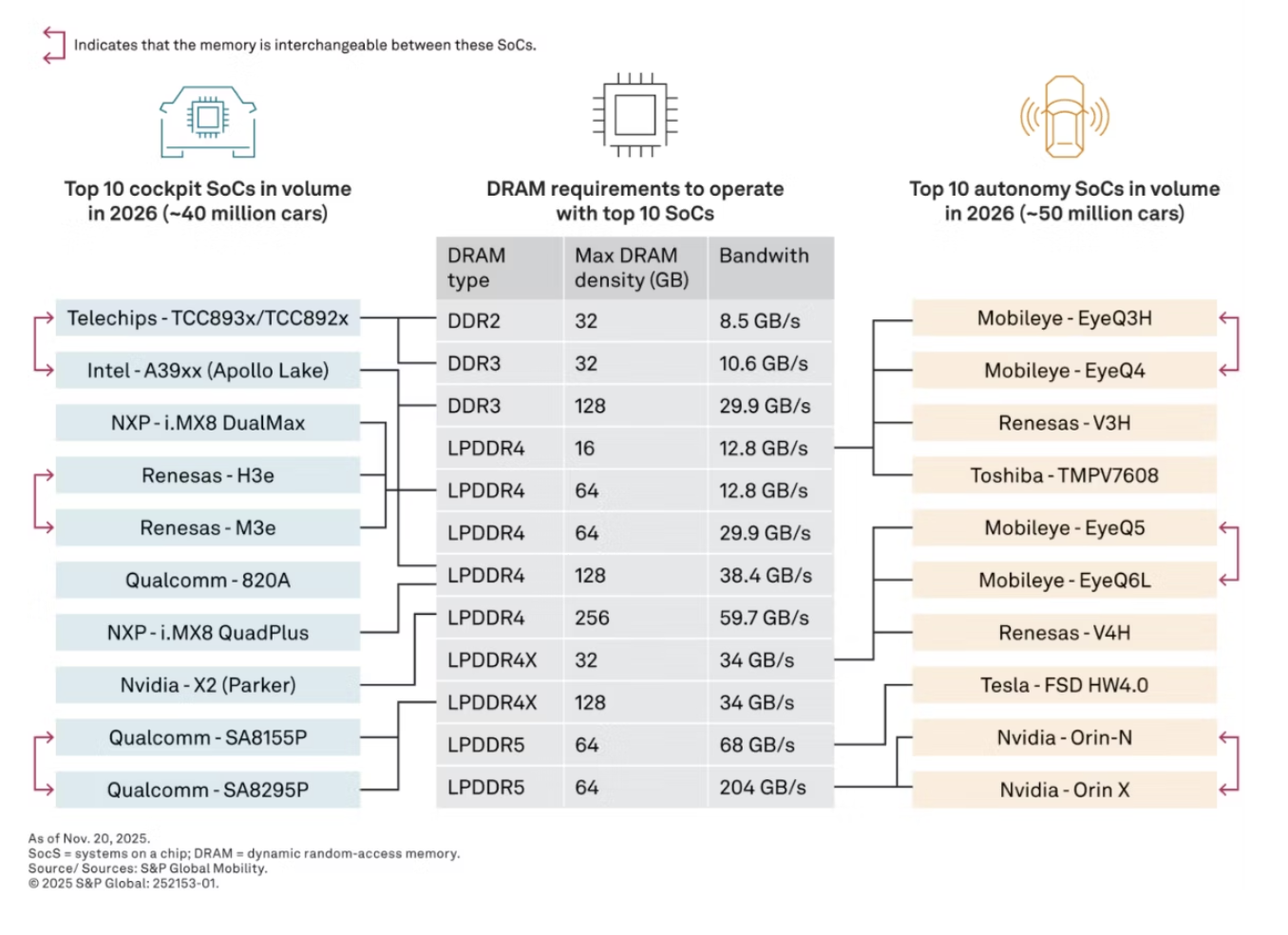

Where DRAM matters in vehicles

DRAM exposure is concentrated in the fastest-growing electronic domains inside modern vehicles:

- Digital cockpit / infotainment (high-resolution displays, multi-screen UX, richer OS stacks)

- ADAS / domain controllers (sensor fusion, perception, mapping pipelines)

According to UBS (citing S&P Global Mobility), DRAM content per vehicle ranges from roughly $25 to $150, depending on electronics intensity. S&P’s longer-form analysis indicates that high-tech vehicles , particularly EVs, 0can exceed those levels, reflecting centralized compute architectures and rising software complexity.

This concentration means disruption risk is not evenly distributed. Vehicles with heavier ADAS and cockpit content face greater exposure to both pricing and allocation shocks.

What “Disruption” could look like in Q2 2026

UBS’s call is less about a single catastrophic shortage on day one and more about a mix of cost shock and allocation shock that can still disrupt production:

1) Cost shock

UBS notes >100% price hikes already being acknowledged by some participants. If those costs cascade through Tier-1 negotiations, the near-term pain can show up as margin pressure and pricing disputes.

UBS also ran a simplified stress case for a “generic supplier” that illustrates the sensitivity: +120% DRAM pricing, with 80% OEM cost recovery, translating to roughly a ~5% EBIT hit in 2026.

2) Allocation shock

Even if parts are technically available, allocation can tighten enough that lead times stretch and “small missing parts” can delay shipments. This is the scenario where automakers aren’t completely shut out — but they are competing for delivery certainty against customers with larger, longer-term commitments.

S&P Global Mobility adds an important “next chapter” beyond Q2 timing: older DRAM generations still used widely in vehicles may face accelerating end-of-life pressure, creating a redesign and qualification squeeze later in the decade.

The highest risk concentrates where DRAM intensity is highest: vehicles and suppliers with heavier ADAS + cockpit electronics content. Several reports summarizing the UBS view point to greater relative exposure for tech-heavy EV programs compared with legacy OEMs that may have more diversified sourcing leverage and larger purchasing footprints.